Personal financial planning for Spain

neto.es calculates long-term projections of your financial future, so you can compare options before making financial decisions.

neto.es is in early access. We are opening the product gradually while we expand supported financial cases.

USE CASES

Demo: Can I retire earlier?

Financial engine for Spain

Your situation

Taxes and contributions

Future decisions

Assumptions

Calculation engine for Spain

The real power of neto.es is in what sits behind the chat: a calculation engine that projects your financial future through thousands of connected calculations. It combines the Spanish rules that matter with your real data: income, IRPF, Social Security, public pension, housing, investments, debts, and liquidity in one monthly model. Each decision flows through the rest of the plan, because the result depends on how all the pieces evolve together over time.

For example: contributing more can reduce your financial room today, but improve your future public pension; buying a home can increase net worth, but leave less cash to invest; drawing from a private pension can cover a shortfall, but increase IRPF. neto.es connects those consequences in one projection, so you can see the full long-term effect.

For you, that means a reliable financial projection, with numbers you can trust as a basis for making decisions.

Simple flow, serious planning model.

One current situation. Multiple scenarios. Month-by-month cashflow, pension timing, net worth, and first-failure-year clarity.

Capture your current situation

Start in chat. The app builds one canonical snapshot of income, expenses, assets, liabilities, and the household context that drives the plan.

Build scenarios

Add structured scenarios with assumptions and planned changes like buying a home, retiring earlier, changing housing strategy, or investing your monthly surplus.

Compare futures

Compare month-by-month outcomes, milestones, pension timing, net worth, and the first failure year before committing to a plan.

Test the plan before life tests it.

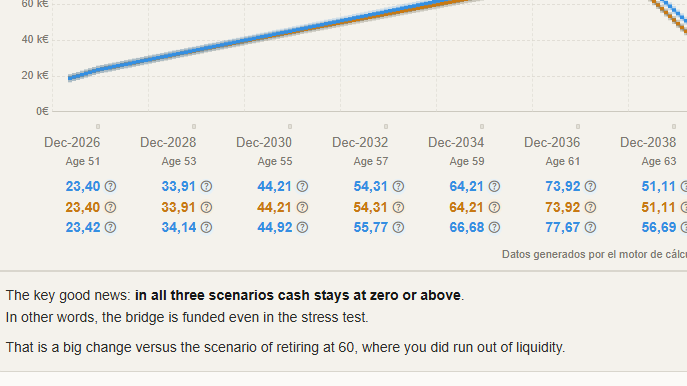

A projection is only useful if you can ask what happens when the future is less convenient than expected. Try lower investment returns, higher inflation, a later home purchase, a salary change, or a larger cash buffer, then compare the result side by side. Stress testing helps you see whether a plan is robust, where it becomes fragile, and which assumptions matter most.

Financial independence from several angles.

They all orbit the same idea: whether your resources hold up once work is no longer required.

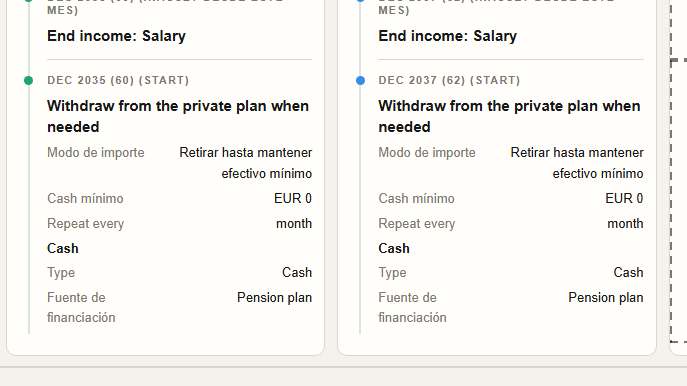

Could I stop working at 60?

Will my money last until public pension starts?

What happens if I reduce my expenses?

What if I rent out my second home?

What happens if returns fall?